Why Pharma companies have no substantial impact on the mHealth app economy

Leading Pharma companies strive, but most of them fail, to have a significant impact on the mHealth app market. In fact, some have released more than 100 public apps available for iOS and Android with which they have generated only limited reach.

The mHealth Economics 2017 Report is out.

Download the report for free!

This is one of the results of the new report “Pharma App Market Benchmarking 2014” which has been published in October 2014.

Each of the leading Pharma companies offers 60 apps in the Apple App Store and Google Play. In comparison, a typical mHealth app publisher that has just 1-2 mHealth apps placed in these stores (see: “mHealth App Developer Economics 2014” free report).

With all these apps, Pharma companies have created only little reach. In summary the leading Pharma companies have been able to generate 6.6m downloads since 2008 and have less than 1m active users. Given their dominant position in the healthcare market, the investment made into app publishing and the spectacular success stories of garage-type mHealth app publishers, the Pharma companies app portfolios’ performance is disappointing.

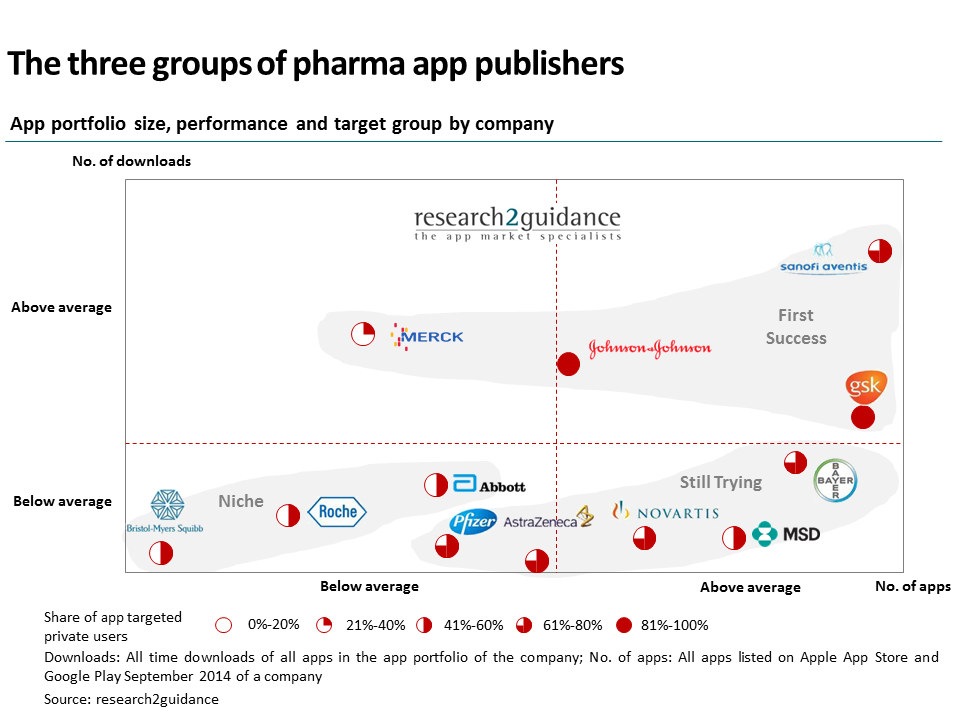

The app publishing activities of Pharma companies differ in size, reach, the use cases (reference, fitness, medical condition management). The Pharma app publishers can be clustered into three groups: The Niche players, the Still Trying, who publish many apps but so far have not been really successful, and, finally, players who have already achieved some First Success.

- Niche: Niche players, for example Roche or Bristol-Myers Squibb, use apps in order to promote their core products. They have a relatively higher share of apps which target healthcare professionals. Their portfolio size and reach is below the average. Focus on apps which target specialized groups of professionals might be an explanation for the lower reach as the potential market size is much smaller than the private app user groups. With their apps which focus on private users, they target women, health tracking or diabetics, all of which represent very large potential user groups.

- First Success: This group represents Pharma companies with a large app portfolio that has generated above average download numbers. The majority of their apps target the mass market of private users. Their portfolio includes one or two apps with a reach of hundreds thousands or, in one case, more than a million downloads. For example, 86% of Sanofi’s reach is thanks to its top 3 (out of its 100 plus) apps.

- Still Trying: This group includes companies like Bayer Healthcare or Novartis. These companies are very active in terms of the number of published apps which predominantly target large private user segments. Despite this mass market focus of their app portfolio, their user reach is low and below average. In contrast to the “First Success”, “Still trying” players have not succeeded in releasing any particularly successful app. For this reason, the share of the top 3 apps in their app portfolio is much lower as compared to those publishers who have already had some success stories.

Comparison and analysis of the app activities of the top 12 Pharma companies gives clear hints why the performance has not been as spectacular as one would suspect.

- The app portfolios are not globally available: Almost 50% of Pharma companies’ app publishing entities target only local markets and are generally available in 3 or less countries.

- The app portfolio is built around the core products of the Pharma companies and not around the actual market demand: By this is meant that if a company specializes in the treatment of hematological diseases, the app portfolio reflects that. In such a case an app would provide references to the latest research findings, support diagnosis and/or facilitate information exchange with and/or between the experts. There is a demand for such products, but other use cases such as health tracking, weight loss, fitness or diabetes condition management, which attract attention of larger groups of users.

- No cross-referencing and common and recognizable design: So far Pharma companies have used neither the potentials of cross-referencing between their apps nor common style guides for their app portfolio. Taking such steps could improve their presence and the corporate identity in the app market.

Other potential reasons why the Pharma companies have not been particularly successful in app publishing is the way Pharma companies organize their app business. In fact, the leading Pharma companies use up to 17 (Novartis) different app publishing entities. A relatively extensive network of app publishing entities means that a globally aligned app category focus and reuse of existing concepts and knowledge is hardly possible.

Finally, Pharma companies should also question their role in the mHealth app economy: is it a good strategy to develop and publish the next 700 apps in the next five years? There are other roles (e.g. mHealth data aggregator, mHealth app incubator, partnering) that might be better suited for Pharma.

There is much more on how Pharma companies make use of the mobile app channel in the “Pharma App Market Benchmarking 2014” report. Read more here

Why do you think Pharma companies don’t succeed in the app economy? Please feel free to share.

– –

NEW: Our report “EU Countries’ mHealth App Market Ranking 2015” is out now. Download it for free.